Health & Fitness

Ensuring Bad Outcomes: What Cyprus tells us about the World

Continuing coverage on the situation in Cyprus - What would happen if another banking crisis happened on american soil, would deposit insurance save us?

by Adam B. Levine

Originally Published March 19, 2013 at endthelie.com

Things are bad all over, worse in Cyprus than most. Earlier today the Cypriot Finance minister submitted his letter of resignation, and it was rejected by the president of the Country. What do you say to that?

Find out what's happening in Napa Valleywith free, real-time updates from Patch.

Backing up a moment, we learned over the weekend that Cypriots would be the latest in the Eurozone bailout parade, but this time it comes with a few twists. For a more detailed account and explanation of events so far, take a look at The Controlled Demolition of Cyprus

Find out what's happening in Napa Valleywith free, real-time updates from Patch.

These are the highlights:

- The largest single portion of the bailout funds will be confiscated from bank accounts of individuals at Cypriot banks

- The Crisis was kicked off by the European Central Bank suspending ongoing financing operations over a holiday weekend. Without that action the banks would have remained solvent and operational until at least June when a large bond payment is due.

- The Deposit Insurance scheme that covers all Cyprus accounts up to 100,000 Euros will not be triggered.

Since we last spoke, the Bank Holiday has been extended from Tuesday to Thursday and the vote has been delayed for lack of support at least three separate times. At this point even the ruling party (the 20 of 29 required votes) is simply abstaining when the issue comes up, not wanting to further tie their political futures to what can only be described as the biggest grab of depositor funds by a non-dictatorial regime ever.

Needless to say, these folks are not popular at home.

Now that things have officially gone to hell and the measure looks unlikely to ever pass, there are some stark realities that will need to be dealt with in Cyprus

- To ensure they would collect the maximum “tax”, the Cyprus government froze all accounts to prevent a Bank Run.

- Freezing all bank accounts so you can steal money from them is illegal

- If the plan passed, it would have been made legal retroactively

- Since the plan now looks like it won’t pass, it’s still illegal, and the hole is getting deeper as the illegal freeze is extended to buy time.

This is a very uncomfortable situation for the Cypriot politicians who were charged w ith implementing this scheme domestically by the European Council and the ECB - It was not their idea, and actually went against the election pledges of the party put in power just a few weeks ago.

An American corollary to this would be Treasury Secretary Hank Paulson bringing the infamous 3 page term sheet to a new congress asking for the blank check that would be TARP. Many steadfast “conservatives” buckled and went along when told “to do anything else would bring disaster.”

The ECB and EU leadership desperately want Cyprus to get on with it because panic is really starting to spread now that the problem is out in the open and the public impression is the plan will fail.

Whether fear or principle (more likely the former) the Cypriots are saying no, and so we’ll all get to see if the threatened apocalypse is fiend or fancy.

Meanwhile, Elsewhere

Events have been met with a variety of non-responses. In the US the ABA (American Bankers Association) issued a statement to assure American depositors their bank accounts are safe, and that Cyprus is a very different circumstance.

ABA Statement on Events in Cyprus

By James Chessen, ABA’s chief economist

“While the crisis in Cyprus is a real concern for depositors in Cypriot’s banks, it has no implication for depositors in U.S. institutions. Depositors in U.S. banks are insured up to $250,000 and no insured depositor has ever lost money in a bank failure. The U.S. banking industry has rapidly returned to health with strong earnings, lower losses and significant increases in capital. The FDIC insurance fund has over $25 billion in reserves and the banking industry – which bears all the financial costs of supporting the FDIC – pays over $12.3 billion each year to assure adequate funding. Simply put, U.S. insured depositors are safe and their deposits are protected by a strong FDIC fund, a financially secure banking system and the full faith and credit of the U.S.

Well that sounds good, after all “Twenty Five Billion” dollars is a lot of money! Of course, the US banking sector is one of the largest industries in the country...

The Cleanup Brigade

So the way this works is if a bank finds itself without enough capital (borrowed or not) to continue normal operations, the FDIC (Federal Deposit Insurance Corporation) takes it over on a Friday, tries to arrange buyers for all the banks saleable assets, and whatever the difference is between the deposits (liabilities) and market value of the assets comes out of the FDICs 25 billion reserve before re-opening on Monday. Hundreds of banks have failed and been subject to this process since the financial crisis got rolling. You can check out the complete list since 2005 at the FDIC’s Failed Bank page

Lets take a look at the most recent name on the list. Frontier Bank of Lagrange, Georgia failed on March 8th, 2013. At the time of closure they officially had $258.8 million in total assets and $224.1 million in total deposits. So at face value, it looks like they had a buffer of $34.1 million between the saleable value and what they owed depositors.

Put another way, if every depositor showed up wanting their money the bank should be able to sell enough assets to raise the depositor cash and still have money left over... And yet the FDIC estimates the cost to them at $51.6 million, which implies that the value of the assets was not 258.8 million, but actually $172.5 million against customer deposits of 224.1 million. That’s a 33% lower valuation than the bank was publically stating, and means they overvalued their assets by 23%!

The next three banks down the list are just as bad.

Bank

Customer Deposits

Saleable Assets

FDIC Cost

96.5 million

97.7 million

20.3 million

76.2 million

22%

Another thing to notice is that none of these assets are being sold on the open market in a liquidation sale as one might expect given the discounts. The FDIC’s entire job is to limit the visibility of bank failures, and the best way to do that is make sure the depositors don’t even notice their bank failed. Standard operating procedure (used in all of these cases) is to sell the failed bank, along with its customers and their deposits, to a larger bank.

What this glosses over is that in each one of these cases the executives of the failed banks are guilty of fraud at the very least, and violations of Sarbannes-Oxley are very possible if they knowingly certified financial statements containing false information, which is obviously standard practice from these figures. The purchasing banks know the game and are only willing to pay what the assets are actually worth, which leaves the FDIC to pick up whatever the difference is while they change the sign at the bank.

So that’s our system now, and if the ABA is to be believed it’s the thing that guarantees no depositor with less than $250,000 can ever lose anything because of their bank.

But we’ve been looking at specific examples, let's take a step back and look at the big picture of banking in the US. After all, it wasn’t one bank or another in Cyprus seeing the effects of confiscation but anyone with an account in the country

What would that do to deposit insurance in the US?

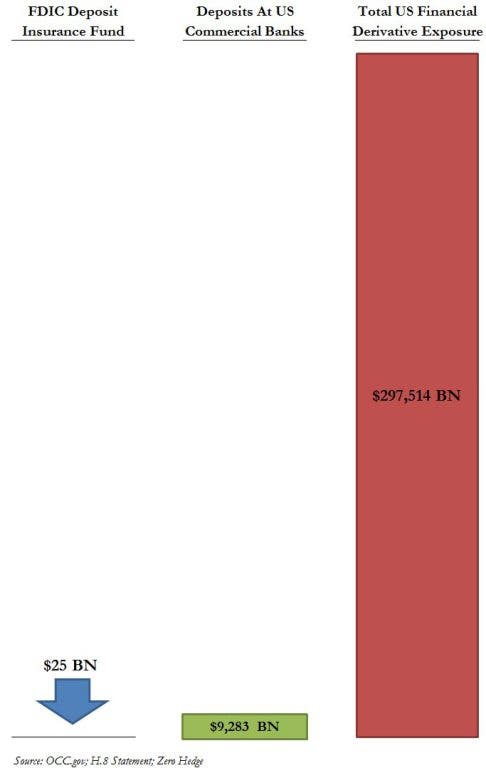

Well that’s a big scary chart. Zerohedge pulled numbers on the biggest 25 banks in and it’s anything but reassuring:

With 9.283 Trillion in depositor funds, it would take only a 0.002% net shortfall in the banking system to completely exhaust the fund. Lets assume the banks want to donate 10 years worth of contribution to the fund all at once, right now. That 145 billion would cover a 0.015% devaluation.

So far we’ve only talked about the tiny blue bar and the little green bar - The big red bar is another animal entirely, and it’s time we addressed him.

In theory, funds deposited with a broker or a bank is still your money. In practice, this is not really the case - Both Knight Capital and MF Global have been caught with their hands in the customer cookie jar after they grabbed whatever funds they could to keep operating for just another day. In the case of MF Global it was a large burst right at the end, but at Knight Capital this was a systemic practice for years.

The problem, as Karl Denninger likes to say, is excessive leverage. In a low interest environment where bailouts are the norm for the largest institutions, there really is no reason to not bet big because if the screw-up is large enough there’s rescue waiting. That scary red bar is the collected debts of those 25 largest banks, and it totals almost 300 trillion dollars, or about 32x total deposits.

I think the chart and numbers say it better than I ever could.

New Zealand on the other hand sees this as a chance to get government out from under the weight of bad banks.

The problem with the FDIC and other deposit insurance schemes like it is that it gives depositors the illusion that their money is safe even if their bank is not. If banks had a track record of acting responsibly this would be alright, but in the real world it means that a bank taking large risks has much more to gain and nothing more to lose than a bank which takes small risks.

It means, basically, that depositors don’t have to care or even know who their bank is, because at the end of the day they’re assured their money will be protected.

The NZ Solution is referred to as “Open Bank Resolution” and it’s very simple - If a bank would go out of business over the weekend, the hole in the balance sheet is filled by scooping the appropriate percentage off the top of depositors’ accounts.

Although at first glance it seems repressive, the more I think about it the more I see the appeal as a participant within the system.

Sounds similar to Cyprus, but it’s not.

Cyprus is a one-off event in the words of those demanding it. It was announced suddenly and people were not allowed to react to this new plan which replaced supposed protection up to 100,000 euros with no protection at all. Since it’s a one-off event, it seems logical to assume that “Deposit Insurance” won’t actually go away in Cyprus, even though when it was most needed it proved worthless.

Compare that to the Open Bank Resolution policy that warns depositors up front to be aware before their bank fails. Suddenly all those depositors have a very good reason to make sure their banking institution is not only taking the appropriate amount of risk, but probably a bit less than that since if something goes wrong, the depositors know it’s coming out of their pocket.

If the results of pervasive Deposit Insurance is to protect bad banks by making sure their customers don’t care, we should see the opposite reaction here - Depositors who will only keep their money in a bank they’re sure is solid.

Rest assured, it will be painful the first few times it happens and if the NZ banking sector is anything like the rest of the developed world it will lead to more than one bank collapsing as its depositors take their money to safer institutions, but the financial eco-system it seems poised to create is compelling, especially as we watch the status quo explode all over itself and those who invest in it.

I’d like to be able to say Cyprus is unique and terrible and completely different from every other country around the world, but it’s a lie and anyone who tells you that is a liar. Cyprus is small and that makes them unimportant enough to be the guinea pig for this crazy, destructive, and ultimately futile move.

But it’s only Tuesday: The week isn’t over yet.

Stay tuned.